When “The Market” Changes: What Proposed S&P 500 Rule Updates Could Mean for Investors

A measured look at proposed S&P 500 eligibility changes, valuation risk, and why technical risk management still matters.

For many investors, the S&P 500 is not just another index. It is the default definition of “the market.” It is where people go when they want broad exposure, low cost, and the feeling that they own the blue-chip core of American business.

That assumption may still be mostly true. But it deserves a closer look.

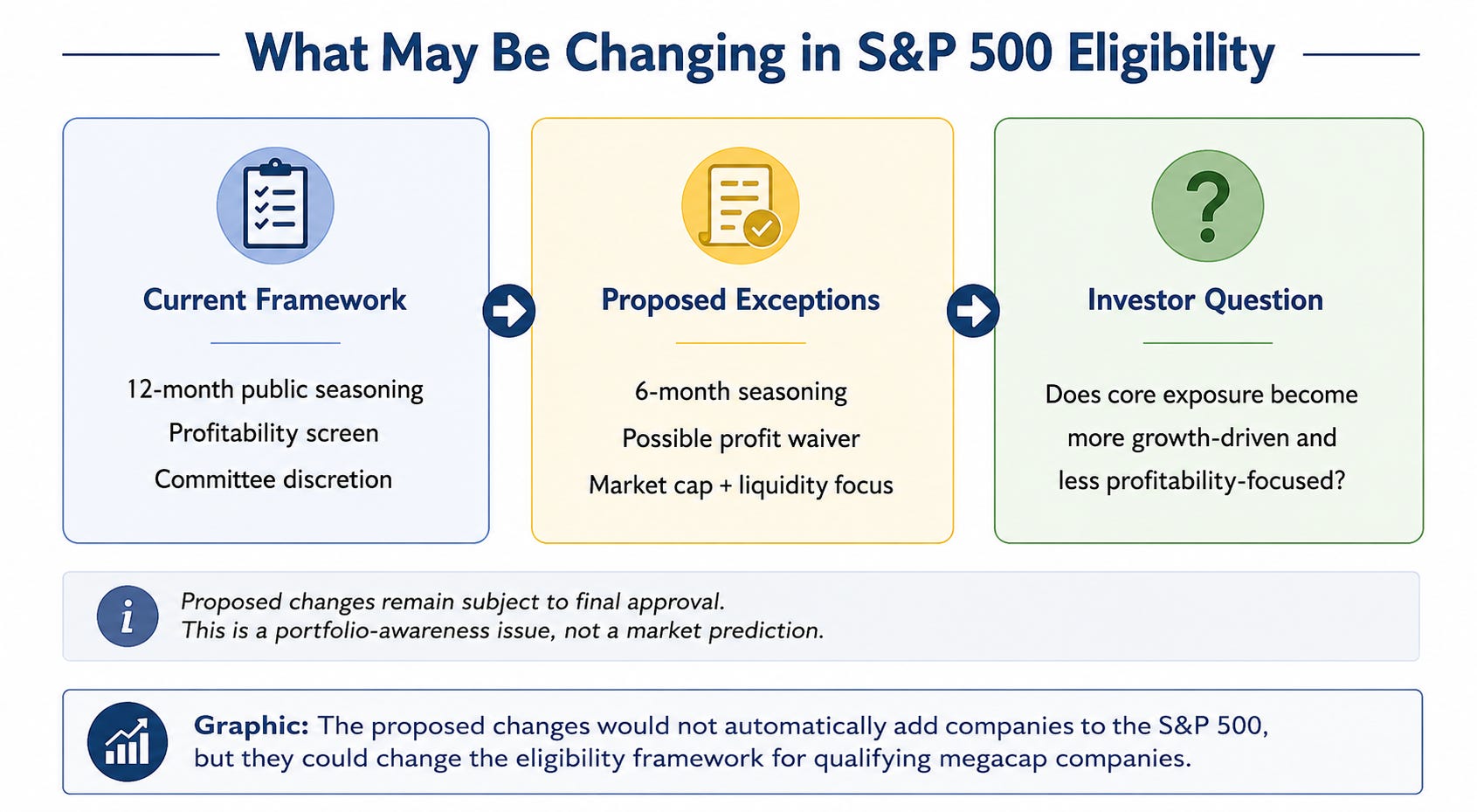

S&P Dow Jones Indices is currently reviewing potential methodology changes that could make it easier for massive newly public companies to enter major U.S. benchmarks, including the S&P 500. The proposal appears designed to address a new reality in public markets: some of the most economically important companies may come public at enormous valuations, but without the traditional profitability profile many investors associate with S&P 500 inclusion.

The proposed changes are not final. That is important. But the fact that they are being considered is meaningful.

According to Reuters, S&P Dow Jones Indices opened a consultation on potential changes to its U.S. index methodology related to megacap companies. The consultation period is open until May 28, 2026, and if changes are adopted, S&P DJI has proposed implementing them prior to the market open on June 8, 2026.

The two key potential changes are simple. First, the seasoning period for a company to be publicly traded before becoming eligible for index inclusion could be reduced from 12 months to six months. Second, S&P DJI is considering excluding profitability requirements for large-cap companies. Other reporting has described this as a potential waiver for megacap companies, allowing inclusion based more heavily on market capitalization and liquidity even if standard profitability thresholds have not been met.

That would be a major philosophical shift.

The S&P 500 has never been a perfect quality index. It is committee-selected, market-cap weighted, and influenced by the same investor enthusiasm that drives all markets. But the profitability requirement has historically acted as a useful filter. It helped reinforce the idea that the S&P 500 was generally made up of seasoned, established, profitable companies.

If that screen is loosened for megacap companies, the character of the index may change. Not overnight or necessarily in a reckless way. But incrementally, and possibly in ways many investors do not fully appreciate.

There is a fair argument on the other side. Companies are staying private much longer than they used to. By the time names like SpaceX, OpenAI, or Anthropic eventually come public, they could already be among the largest and most relevant companies in the world. If an index is supposed to represent the market, then excluding companies of that size for too long may make the index less representative.

Nasdaq has already moved in this direction. Its new Nasdaq-100 rules took effect on May 1, 2026, and under its fast-entry rule, a newly listed company that meets eligibility criteria can be added after the 15th day of trading. That is a very different world from waiting months, or potentially a year, to see how a company trades, reports, and handles public-market scrutiny.

So, this is not about saying index providers should never evolve. They should. Markets change. Company structures change. Public and private markets change. The real question is whether investors understand what those changes may mean for the portfolios they already own.

That is where the behavioral side matters.

Many investors buy S&P 500 funds because they believe they are getting disciplined, diversified, blue-chip exposure. But if the index begins making room for enormous, less seasoned, potentially unprofitable companies at very high valuations, investors may still think they own the same thing while the underlying risk profile becomes incrementally more growth-oriented, more narrative-driven, and potentially more speculative.

That does not mean those companies are bad businesses. Some may become extraordinary long-term winners. It also does not mean investors should avoid the S&P 500. The point is awareness. Passive investing does not mean the index is passive. Rules, committees, and eligibility criteria matter.

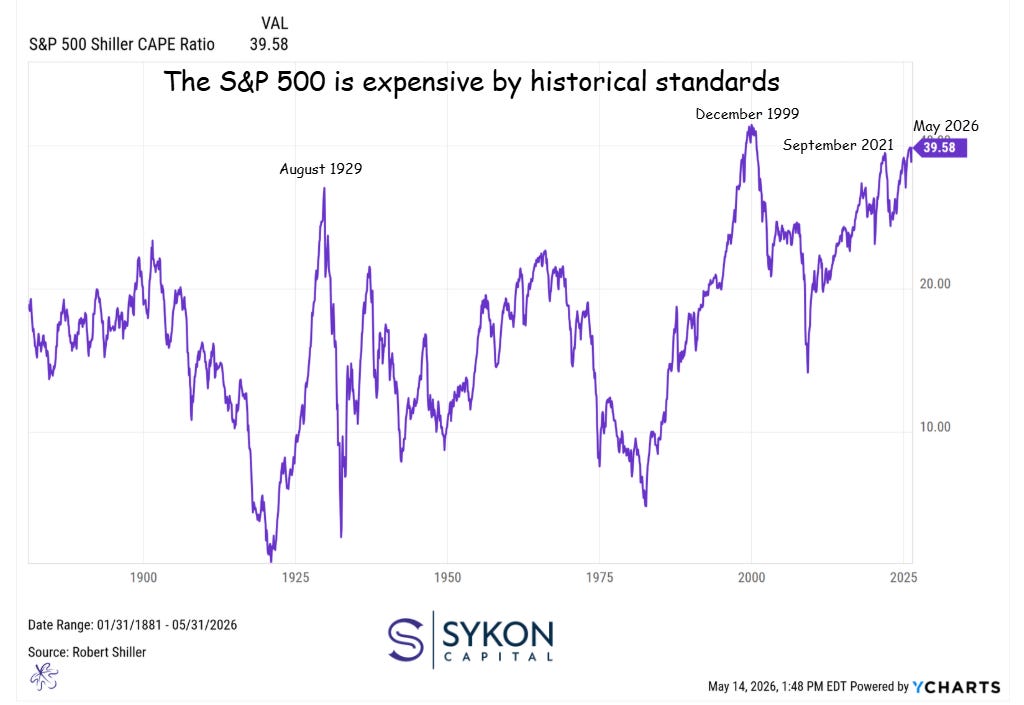

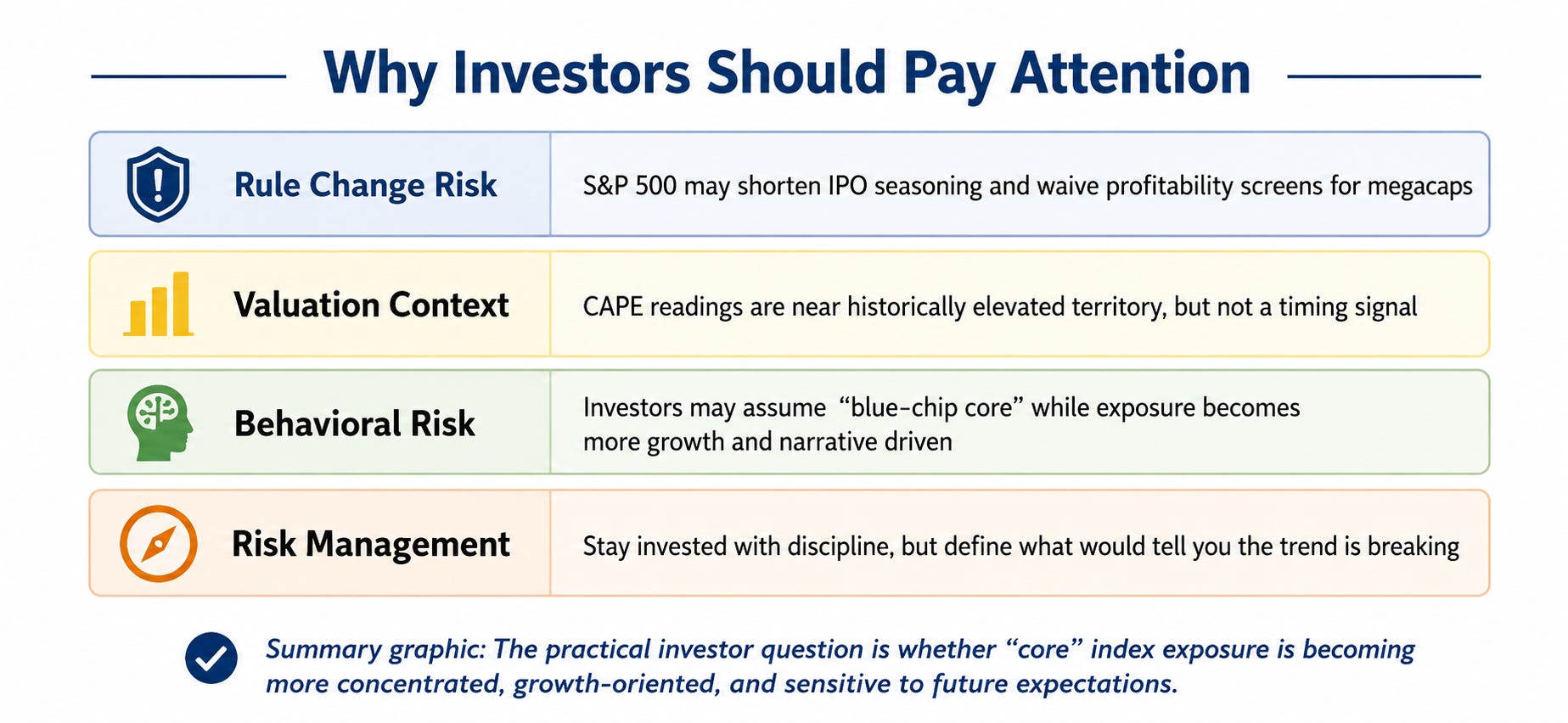

The timing is also worth discussing because valuations are already elevated. The Shiller CAPE ratio compares the S&P 500’s price to a 10-year average of inflation-adjusted earnings. Different providers calculate and update the figure slightly differently, but recent readings are clustered around historically high levels. Multpl showed a current Shiller PE ratio of 38.94, while GuruFocus cited a Shiller PE near 40.3 in May 2026. Multpl’s historical table also shows 43.77 in 2000 and 40.57 in 1999, near the dot-com valuation extreme.

Chart: CAPE remains near historically elevated territory. This is not a timing tool, but it is useful valuation context.

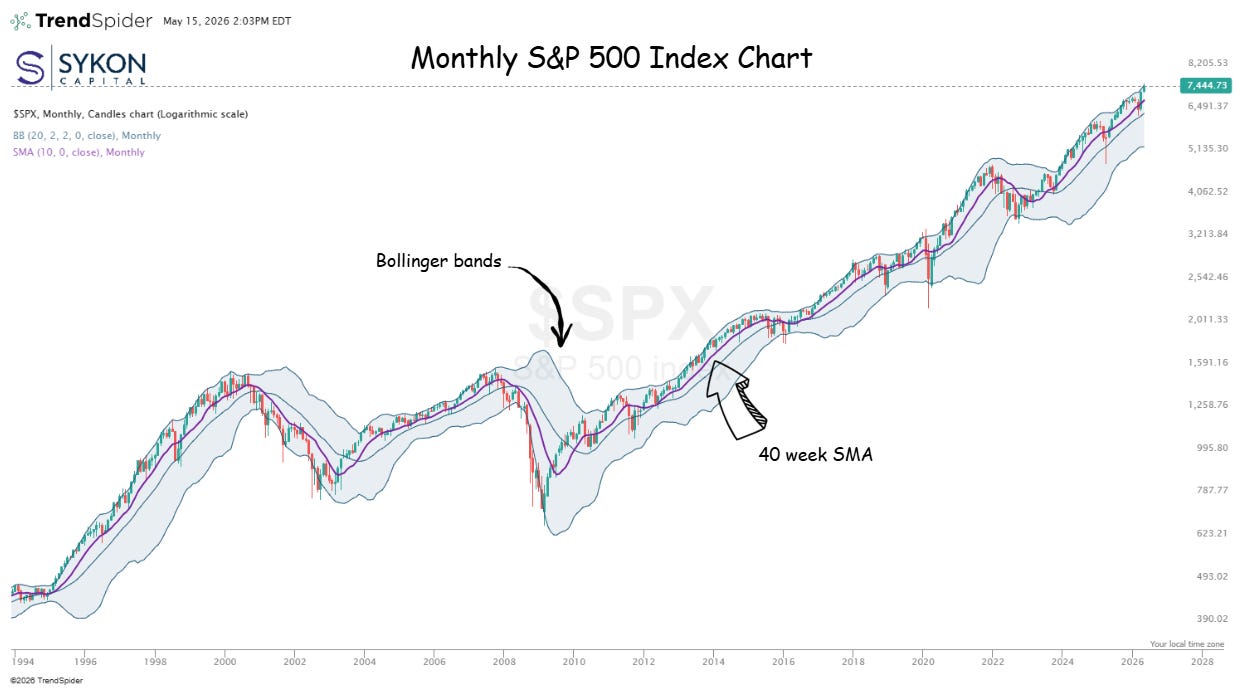

This is not an alarmist point. High valuations do not tell you when a market will turn. They do not mean a crash is imminent. In fact, the current trend of the S&P 500 index remains constructive, especially when viewed through a longer-term monthly technical lens. Strong markets can stay strong longer than many people expect.

But that is exactly why risk management matters.

When a market has delivered an epic bull run, the goal is not to call the top every week. That is not a process. The goal is to participate in the trend while having tools that help identify when the character of the market is actually changing. There is a big difference between respecting momentum and ignoring risk.

This is where technical analysis can be helpful. A monthly chart of the S&P 500 can help investors separate noise from meaningful deterioration. Are prices holding key moving averages? Is market breadth confirming the index? Are leadership stocks still leading? Are momentum indicators deteriorating while prices make new highs? These are the kinds of questions that matter when valuations are high and index construction may be shifting toward more speculative exposure.

Chart: The S&P500 trend remains positive, but risk management means knowing what would change that view.

The risk is not simply that the S&P 500 adds a famous unprofitable company. The bigger risk is that investors do not realize how much their portfolios may already depend on the same growth, technology, AI, and megacap themes across multiple funds. An investor may own an S&P 500 ETF, a Nasdaq-100 ETF, a large-cap growth fund, and an AI-themed fund and believe they are diversified. In reality, those exposures may overlap more than they think.

That is why this conversation matters. Not because investors should panic or because a rule change automatically breaks the market. But because the definition of “core” exposure may be evolving at the same time valuations are elevated and investor enthusiasm is concentrated in a narrow set of themes.

The practical takeaway is simple. If you own the S&P 500, know what you own. If you own multiple index and growth funds, understand your overlap. If you are comfortable riding the bull market, have a plan for what would tell you the trend is weakening or shifting.

This is not about being bearish. It is about being disciplined.

Markets reward participation, but they punish complacency. The S&P 500 has been one of the most successful investment vehicles in history because it gave investors broad, low-cost exposure to American corporate growth. But if the rules evolve, investors need to evolve their understanding too.

The market may be changing what it means to own the S&P 500. The most important question is whether investors realize it before the next cycle tests that assumption.

Why This Is Worth a Real Portfolio Review

This is also where I think investors should be selective about who they ask for guidance. This is not just a financial-planning question. It is a portfolio-construction question.

At SYKON, this is not an abstract discussion. Our work centers on portfolio construction, market structure, index methodology, and technical trend analysis. We evaluate how rules, flows, and investor behavior shape real-world exposure. That investment focus allows us to identify risks that are often invisible at the asset-allocation level but highly relevant at the holdings level.

If you want help understanding how much of your portfolio is tied to the S&P 500, Nasdaq-100, large-cap growth, AI, or overlapping megacap exposure, ask us to look it over. If not us, get an informed second opinion from someone who understands portfolio construction, not just passive allocation. The point is not to overreact; it is to pay attention before the market forces the lesson.

The S&P 500 may be evolving. The most important question is whether investors evolve their understanding with it.

Quick Answer for Readers Searching This Topic

S&P Dow Jones Indices is reviewing proposed methodology changes related to megacap companies and major IPOs.

The proposal could reduce the seasoning period for eligible IPOs from 12 months to six months.

S&P DJI is also considering exceptions to profitability requirements for large-cap or megacap companies.

The consultation period runs through May 28, 2026, with possible implementation before the market opens on June 8, 2026, if adopted.

Potential beneficiaries could include large private companies expected to come public, such as SpaceX, OpenAI, and Anthropic, although inclusion would not be automatic.

S&P 500 rule changes, S&P 500 profitability requirement, S&P 500 IPO seasoning period, S&P 500 megacap IPO inclusion, SpaceX IPO S&P 500, OpenAI IPO S&P 500, Anthropic IPO S&P 500, Nasdaq-100 fast entry rule, Shiller CAPE ratio 2026, index investing risk, portfolio overlap, technical risk management.

Sources and Verification Notes

S&P Dow Jones Indices consultation timing and proposed implementation date, Reuters-linked summary: https://longbridge.com/en/news/284845425

Reuters via MarketScreener: S&P DJI considering six-month seasoning and excluding profitability requirements for large-cap companies: https://uk.marketscreener.com/news/s-p-dow-jones-indices-considers-new-index-rules-as-mega-ipos-loom-ce7f58d8d18bf52d

Bloomberg Law: S&P weighs shorter public-seasoning period and possible profitability/liquidity waivers: https://news.bloomberglaw.com/securities-law/s-p-weighs-new-index-rules-to-speed-up-addition-of-mega-ipos-1

Reuters: Nasdaq fast-entry rule, 15th trading day, and May 1 effective date: https://www.reuters.com/business/new-nasdaq-rules-include-fast-entry-new-listings-benchmark-index-2026-03-30/

Nasdaq: Nasdaq-100 methodology update rationale: https://www.nasdaq.com/newsroom/nasdaq100-index-methodology-update-why-now

Multpl: Shiller PE historical table and current readings: https://www.multpl.com/shiller-pe

GuruFocus: Shiller PE current valuation context: https://www.gurufocus.com/shiller-PE.php

Advisory Services offered through SYKON Capital LLC, a registered investment advisor with the U.S. Securities and Exchange Commission. This material is intended for informational purposes only. It should not be construed as legal or tax advice and is not intended to replace the advice of a qualified attorney or tax advisor. The information contained in this presentation has been compiled from third party sources and is believed to be reliable as of the date of this report. Past performance is not indicative of future returns and diversification neither assures a profit nor guarantees against loss in a declining market. Investments involve risk and are not guaranteed.